Time for a wee break. In the last week, I've been researching Zara and H&M a little, to better understand the retail-sector and the fashion-segment. I'll probably have to do a follow-up to this post, as there is lots to say about both businesses, but here's some initial impressions, nevertheless.

Time for a wee break. In the last week, I've been researching Zara and H&M a little, to better understand the retail-sector and the fashion-segment. I'll probably have to do a follow-up to this post, as there is lots to say about both businesses, but here's some initial impressions, nevertheless.

First off, H&M appears a lot more clean in its approach. Judging by the annual reports alone, H&M not only has a 2007-edition (Zara is only up to 2006), but it is also only 85 pages long (presented in an eco-friendly 2-pages-per-side way), while for Zara, or actually Inditex, it's mother-company, the annual report is a stunning 450 page long!

Now, that's really not all that surprising, as Inditex is composed of a number of companies, and it is extremely vertically integrated, while H&M employs the Nike or Apple model—it designs and it retails, but it doesn't produce.

Why this is so, I can only guess, is due to their origins. Inditex comes from Spain, traditionally a low-waged country, while H&M is Swedish, not a low-waged country. Similar to IKEA, I imagine it was an economical decision to outsource most of its supplies.

It's very hard to separate Inditex from Zara, as both are founded and owned by the same person, Amancio Ortega Gaona, Spain's richest man. Zara has been in existence since 1975. H&M was founded by a Swede, Erling Person, in 1947, who ran the company to ca. the mid-90s, but which has continued to be a family firm.

Their business-philosophies are fairly similar, a low-cost, high-quality approach to fashion, as opposed to traditional brands, where quality most often equals price.

Zara made lots of headlines with its extremely high turnover of products—it produces around 11,000 items annually (as oppsed to 2,000-4,000 for other retailers); 15-20% produced before, 50-60% at the start of the season, and the rest during. If a product fails to do well, it is usually removed after a week in stores.

H&M made headlines with its celebrity-marketing, which is noteworthy, as Zara has virtually no marketing. Instead, because it has such a high turn-over of goods, customers tend to visit it more often, expecting new things—an average of 17 times per year vs. 3 times for other stores!

Both employ mostly a wholly-owned retail-strategy, except in countries where this is not possible. And both are very advanced in their use of IT to manage logistics and production, which is definitely seems to be a key-characteristic of delivering fashion quickly and find ways to decrease costs.

H&M's largest markets are Germany, Sweden, the USA, Spain, and the Netherlands (in terms of sales). For Zara it is Spain, France, Germany, and Mexico (in number of stores).

That's all I can think of in 30 mins or less…

Take a look at this quote, which I posted a few days ago:

Take a look at this quote, which I posted a few days ago:

"There should be a rule: before helping the environment in one market, we should be required to think through the impacts on other markets." (source: Freakonomics blog).Or, to put it differently, every action has a (sometimes equal) reaction (I think the traditional phrasing ignores the human element). The idea that everything is interconnected is both fun to right-brained generalists like me (not a compliment), and scary at the same time. The global economy is very complex and, I would say, impossible to regulate.

There's a couple of things going on the world, which I'm sure everyone is aware of. There's a number of wars, there's the weakened dollar, there's some kind of housing-related recession going on, there's a shortage of oil, our planet is perceived as suffering and currently being saved (I hope), there's India and China, the rise of the Anglo-Saxon system, etc. etc.

And some of the biggest problems facing the food-industry (depending where you are in the chain), are rising food-prices, which relates to that oil-shortage (both in terms of pricing, but also because of alternative fuels using farm-products), the rise of India and China, and some other factors; and the costs of keeping green, which has largely been inspired by companies like Wal-Mart, but also by the (exaggerated) need for global diversity by customers (which the food-industry is also partially to blame for).

The solutions vary, and are, so far, very defensive in their nature. For the cost of going green, most pollution comes from transport and the solution is to either use the most eco-friendly way to go: on land, by train, across water, by ship; or to go local—which companies like Marqt seem to focus on, but which also comes with the pitfall of seasonal shortage.

For rising food-prices, again one solution is to go local, to save on transport and have some control over how farmers work, and be able to charge higher prices to the rising local-conscious consumer. But a bigger solution is for more food-production to happen (much of it currently goes to India & China, or to biofuels), and possibly from smaller farmers. The problem here is that it will take time (some estimate decades) for smaller farmers to get ready.

Both are definitely big picture-problems, and will take time to solve. One thing, I'm personally looking at, are micro-lending sites like Kiva.org, which put you into contact with local farmers, allowing you to help them out in your own way. From a Venture Voice interview with one of the founders, I understand that some of these investments happen within the context of a community, where each member keeps watch over the other's use and repayment of the funds, in order to ensure a good outcome, and so loans will continue to come in. But, while I think it's well worth the effort, this is still a small-picture solution to a much larger problem.

The way it looks right now, the solutions have to be planned in the long-term and on a large scale. There is definitely space in the farming-segment for more production to happen. In the mean time, food-prices will continue rise, as will the price of educating consumers to make more responsible choices. I like Tesco's approach in labelling the origins of their food and allowing people to make more carbon-friendly (locally focussed) decisions. But that doesn't solve the problem for farmers in remote areas of course.

Sigh, if you just got a headache, I sympathise, as I just got one too.

Further reading:

- NYTimes: Environmental Cost of Shipping Groceries Around the World

- Economist: The new face of hunger

- Buzzfeed: Food Hoarding

This wrap-up covers material up to April 6th, 2008. I will dedicate another one to this month and then hopefully go back to a monthly schedule. Looking backwards is hard, but I find it useful…

This wrap-up covers material up to April 6th, 2008. I will dedicate another one to this month and then hopefully go back to a monthly schedule. Looking backwards is hard, but I find it useful…

Normally this would be a monthly wrap-up, except I postponed it by quite some time. In this post, I try to look back in order to see how far I've come and bring a general set of themes to what I've covered so far.

Tag: The internet

I spent a considerable amount of time writing about the internet, somewhat influenced by my thesis and that I've been blogging for longer on Tech IT Easy.

One thing I looked at extensively was social networking, because, hey, that's the age we're in. I looked at lifestyle-brands, which require a more contextual approach, and how the internet can act as a platform for business to communicate with customers more richly and bi-directionally. A related topic—social network as competitive advantage—was published on Tech IT Easy. At the same time, I don't completely embrace social networking like Facebook, which I'm bearish on and have, to a degree, sadly been proven right.

I also looked at the role of the internet in terms of physical retail, for which a company, called NearbyNow, is offering an interesting service to both retailers and consumers; they allow consumers to browse and reserve goods through the internet or their mobiles, and give more exposure to retailers. At the same time, my outlook for the physical retail of media is bleak, and I expect all of it to go via the internet soon.

Tags: Logistics & green tech

In terms of logistics, I looked at different methodologies of storing and transporting goods across the globe. Very interesting how each continent/country is getting around its disadvantages (e.g. high labour costs in Europe) and compensating with other factor (e.g. more technology in European warehouses = less labour dependancy).

Also green tech is another "trend," well, I expect it to stay around for quite some time. I outlined five reasons why I think business are and should be going green. The mirror-post on Tech IT Easy spawned some interesting discussions.

Tag: Business strategy

Of course, business strategy is somehow involved in all business-topics, nevertheless I did look at a number of issues specifically. One was on entry-strategies into difficult markets, which is something I can't really describe in a few words, but requires speed, stealth, and brains.

I also commented on new business developments in a number of retail-outlets, and how it is only those that are synergetic with a company's core-focus, and can reap advantages like scale & scope, that end up being worth the effort.

Not to forget, I wrote about IKEA again, first, in note-form, talking about the international moves that the company made and why; and second, a summary of the lessons that I learned from IKEA.

Finally, I looked at the social element, human resources, and how companies use coaching and social operating mechanisms to scale their strategy and passion across the organisation. Ford, again, makes an interesting case study for that.

Tag: Entrepreneurship

As always, and somewhat difficult to separate from the above. I looked at the interdependent components of strategy, and financial, organisational, and product-market strategies are really part of a greater whole, when writing your business-plan.

I also looked at some statistics in franchising, and the lower failure rates are one reason to consider it a worthwhile entry-point into the industry. Still, it's not risk-free; There's clearly a lot of work to do beforehand, in terms of choosing the right franchise with growth-potential, financial risk to fund your business, market-risk, when you launch, and competitive risk, after your up and running. Some of this should be overcome with the help of a franchiser, however. Related to this, I posted an overview of the week of a franchise-owner, which was quite diverse and exciting, as well as a look into the drugstore-industry in the Netherlands.

On a softer level, I believe that entrepreneurship is ultimately an exercise in focus, which goes so much easier when you love what you do, but also an exercise in believing in the impossible, even when "facts" may prove you wrong. Micheal Masterson also had some good tips for starting & running companies, more from an investor's perspective.

Tags: Branding & marketing

Again, I already linked to some related post under the internet-heading; I believe that social networking is a big deal in that area these days. Related to this is also the concept of referential marketing value, as opposed to direct marketing value, which wrote about a little here. Clearly this is a dimension that is fairly complex but which the figures show should not be ignored.

I also criticised cinemas' moves into the luxury-segment as faulty branding, because luxury isn't a big differentiating factor during the movie-viewing experience; technology and timing is.

Tags: Food and retail

I could've probably placed these in any of the above categories, but this is after all the food and retail blog. I still take a dual approach here, looking at food-retail through retailers, and then through actual food-venues, like restaurants. There is a difference, but I'm not sure whether I want to or should discriminate between them.

In terms of supermarkets, I discussed a number of worrying trends going on in that world, namely there's less consumer-spending on food and supermarkets are forced to respond by consolidating and pushing efficiency up on the agenda. But I also find the presence of supermarkets like Marqt encouraging and hope they do well.

Also, I recently summarised some points I got from a book on Ahold. It's an interesting company to follow as it's been around for about a century, and has survived several similar challenges, we are facing today (high fuel-prices, recession, etc.)

I also discussed snack-food, which I find particularly flawed in terms of health and which could use an influx of alternative, yet good-tasting snacks.

And I looked at restaurants, which I find scary, but I remain open to. Starbucks level of vertical integration is also a little worrying. It's a like a beast that, as soon as it had to retrench from the market, it eats up more companies from the supply-side, in order to gain a competitive edge over other coffee-retailers. There's just something that worries me about this move.

Finally, I took notes from a very interesting lecture by John Schneeberger, who offered some interesting insights into the world of vegetarianism, organics, and local produce.

Other

Other topics that I didn't mention here, include my links (where I try to link to interesting stories) and my interludes (where I try to write about more fun and personal stuff).

Thoughts (written at the beginning of April!)

There's two challenges ahead, as far as my blogging goes. Topic-wise, I'm fairly open to both big-company and small-company problems, which may be too broad. I also perhaps don't focus enough on food & retail in particular, though that's because I'm a generalist and am still deciding on my passions.

Presentation-wise, I've been analysing some other people's blogs, e.g. TechCrunch's & Jeremy Fain's early days, to see what these guys did different. TechCrunch used a very mechanical approach, the same template for discussing companies, no colourful language, and a regular pattern of several posts a day. Jeremy also blogged a lot and brought information to the table that he himself came up with or that he got from discussions with people.

I do too little of that, because I don't make enough time for it and am more introverted in my approach. I can't really say whether my approach will change from now on, but I'll try to bring more of my personal experiences into posts. Those appear to get a better response (still working on that).

A VC: From Messes To Successes:

"The prescription for turning these messes into successes is really pretty straightforward. You need to build the team and bring in people who excel at the blocking and tackling and the PLANNING that most startups don't have the time or inclination to do. And you need to gradually change the culture of the business from one that is all about the product to one that is about the entire company. Sometimes, often times, that means changing the people around. And that's never easy. And it's even harder to change the people around when it was the initial team that made the product so popular in the first place. So you have to somehow find a way to add the 'operational' people without drowning out the 'product' people."

Eggbeater: Chef Owners Who Work The Line

I'm starting to think people should take a test before they open a restaurant. It will be like a triathlon: you must work the line, well, if not stellar. You must understand and be able to explain one P&L statement. You must understand why raw fish and cooked meat cannot share the same bin in the walk-in. You must understand how to make cookies, one dessert with chocolate that's not a molten chocolate cake and it would be great if you knew the difference between panna cotta and creme brulee. The test would list a series of questions and you would be graded on how much responsibility you took for your own actions or the actions of those you hired. For bonus points you might have to research why all the restaurants in your location before yours failed, or cooking in and creating a menu for a kitchen with no Latinos (or your State/ Country picks for easy-to-exploit-able peoples.)

Freakonomics: The Consequences of Being Green

There should be a rule: before helping the environment in one market, we should be required to think through the impacts on other markets.

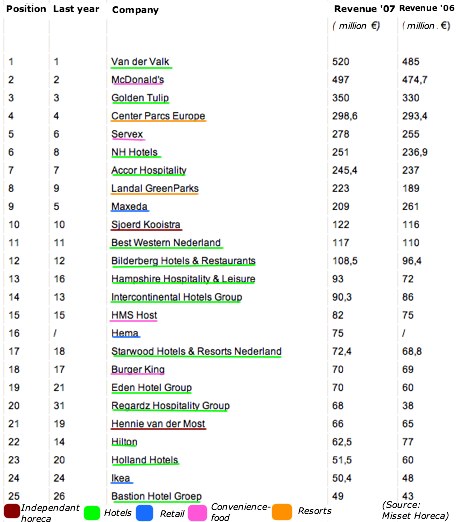

I've included just the top-25 and annotated their focus. What's interesting, but not surprising, is that the majority of companies in that list are not independent horeca-orientated, apart from two: Hennie van der Most and Sjoerd Kooistra, both Dutch horeca-entrepreneurs.

The majority is hotel-chains, though the top-10 is quite diverse; a number of convenience-(fast)food places, resorts, as well as retailers. Interesting that both Ikea and Hema are on that list. Hema, as far as I know, has not been on the horeca-market for long (no revenue reported in 2006), but is already reaping significant successes. Probably my favourite retailer in the Netherlands, btw. Ikea, as I reported before, has been in the restaurant-business since 1971.

You can see the complete top-100 at Misset Horeca.

I'm thinking about adding another "interlude" to my collection, inspired by ADD without a doubt. It's the cookerlude, baby, aimed at collecting thoughts and notes on cooking in order not to forget and to better understand the world that a cook goes through. While I cook nearly every day, I don't consider myself a good cook. I simply don't have the taste-buds for it; but I do love the good food, which, luckily, my gut no longer shows!

I'm thinking about adding another "interlude" to my collection, inspired by ADD without a doubt. It's the cookerlude, baby, aimed at collecting thoughts and notes on cooking in order not to forget and to better understand the world that a cook goes through. While I cook nearly every day, I don't consider myself a good cook. I simply don't have the taste-buds for it; but I do love the good food, which, luckily, my gut no longer shows!

I recently discovered a podcast, called/by The Restaurant Guys, which, apart from the insanely long commercials, actually seems quite interesting and is funny enough to keep my attention. Some notes.

Salt: So, we seem to have this internal taste-meter for the stuff, which in some ways is tied to the percentage of salt in salt-water. At the same time, our saliva actually dilutes salt in food, reducing it, meaning there should be a higher percentage in food than salt-water, for us to enjoy it.

Sugar: apparently there's no set limit for that, people love sugar (I must be the exception).

Salt + Sugar: whenever you make a sugary desert, adding a little(!) salt helps the taste; apparently they do funny stuff to each-other in your mouth, a party in your mouth, so to speak.

Taste-enhancers: apart from the above, olive oil, mushrooms, garlic, tomato-paste, alcohol (and much more) enhances the taste in your mouth.

Pretty basic, no? You can listen to the whole episode on what (American) people like in their food, here.

My own world

(This is where I talk a little about what I discovered myself in regard to cooking. Pretty basic too, so I'll try not to embarrass myself.)

I'm a big fan of salads, I make and eat one nearly every day as a meal. I often use canned tuna, but I recently discovered salmon in a can, which tastes better, is less salty, healthier, and costs about the same here in the Netherlands.

But steamed salmon is the best. You can get an expensive steamer, but a cheap solution is a microwave-steamer. I found one in a Chinese store for about €10, you can steam whatever you want in 5-10 mins and it magnifies the taste. Add some green beans and carrots, and you got a great salad for a meal! Add some potatoes or rice, and you won't need the salad.

Last, but not least, sometimes, not always,Ketchup actually makes for an interesting dressing (together with some oil and spices). It often contains vinegar, which salads like, and the tomato mixes well with the salmon-taste.

That's about it for today, I'm not sure how often I'll repeat these cookerludes, but I hope you enjoyed it! The picture is of course of Chef!, the show.

Interlude: From medical to space-tech - How technology affects incubation-strategies

0 comments Posted by Unknown at 8:48 AM High-tech… My never-ending hobby! Read about it on Tech IT Easy!

High-tech… My never-ending hobby! Read about it on Tech IT Easy!

I took part in a "flirting in business" workshop last night, pretty fun and insightful. It tried to explain the fundamentals of communications to us—around 50 professionals, students, work-seeking-people, etc., both shy and outgoing, all with their own qualities and questions—and I took a lot home from it, including a book by the presenter.

I took part in a "flirting in business" workshop last night, pretty fun and insightful. It tried to explain the fundamentals of communications to us—around 50 professionals, students, work-seeking-people, etc., both shy and outgoing, all with their own qualities and questions—and I took a lot home from it, including a book by the presenter.

So, apparently a "flirty" conversation has three main components:

- giving attention;

- showing curiosity;

- showing trust.

Several things, like conditioning, fear, and ego stand in the way of change, and the only way to get around it, is to acknowledge the feeling as it happens and know that you have a choice. Good to know! Apparently, a conditioned change—one that lasts—can happen quite quickly, you have to practice it around 15 separate times for it to become internalised.

A round of answers were given concerning what people pay attention to during a first meet, the infamous first impression: it ranged from dry hands (which you can't do anything about), tone of voice, general looks, and, most importantly, the smile, as that overcomes a lot.

It was also interesting to hear that only 7% of the message that we get from people is verbal, and the rest is sensory. That explains why I often don't listen and go on instinct, I guess… :)

Did I take anything big back from that meeting? Not really, except that it's really not that hard to sell yourself, as long as you have a certain awareness of what's going on in your head and what matters to other people.

Dear reader,

Dear reader,

If you've been following my blog, which is kind of you, you may have noticed both a drop-off in posts, and, more importantly, a drop-off in relevancy.

To put it bluntly: I'm bored of the topic! I've been researching this industry to the extent that everything seems similar, rising food prices, fmcg-marketing strategies, the "organic" differentiator, etc. etc., it all feels like I've seen it before, and I'm struggling to come up with new and interesting topics.

In addition to this, and this is entirely my fault, I'm stuck with a project that doesn't want to finish itself, my thesis that refuses to get published, or rather that I refuse to be published. The effect is that I'm sitting behind a PC… a lot… and not experiencing/talking with insiders/etc. enough to get fresh perspectives on the field of "third places" and feel productive in that setting.

I'm not going to abandon this blog; no, very likely I'll continue to publish several posts per week. However, some, if not all, will not exactly be on topic; they will likely be discussing things going through my mind, on business, on art, on technology, etc. and hopefully on sounds + food 'n' retail as well.

Until I dig myself out of this valley, and I will, I hope you'll be patient and not hold my lack of focus against me. I still aim to be a producer of excellence in mine and your world.

Sincerely,

Vincent van Wylick

Main honcho @ foodandretail.blogspot.com

- Starting with a lecture by Robert J. Sawyer, regarding the difference between Star Trek & Star Wars. I had no idea that the phrase "A long-long time ago, in a place far-far away" makes such a big difference. Essentially, while science fiction was originally a commentary on issues in our own society, that phrase gave George Lucas the license to not-comment, or rather to accept things like racism (towards robots), slavery (robots again), and countless of other stuff. Really a good lecture to listen to, if you're into sci-fi.

- On a related note, I recently (re-)watched Star Trek 1-6. You really notice the shift from slow cinematics in Star Trek 1 and 2 (a la Kubrik's 2001, which I'm not a fan of), followed by more intense action-scenes in the later ones. I think I recorded the social values more on a sub-conscious level. Numbers 4-6 were my favourite, regarding nature (transporting whales through time); the search for God; and retirement. But I have to say, Kirk was at his strongest in the first two movies. Also, something else I didn't know: Leonard Lemoy (Spock) is a multi-talented individual: writer for several films, producer, and of course actor.

- My favourite adventure movie these last few months: Lawrence of Arabia.

- My favourite cartoon: The girl that leapt through time.

- My favourite fantasy: Pan's Labyrinth (picture is my interpretation of Pan)

- A film, which is taking me a long time to watch, but which I will finish because it's good: Francis Ford Coppola's Youth without Youth.

- Excellent commercial, but not mainstream, movies: Into the Wild; There will be blood; No Country for Old Men (the last three, somewhat depressing too); and Juno.

- An excellent series that recently finished and everyone should watch: The Wire. Seasons 1-4 especially.

- An series with potential that will hopefully not be cancelled: The Sarah Connor Chronicles.

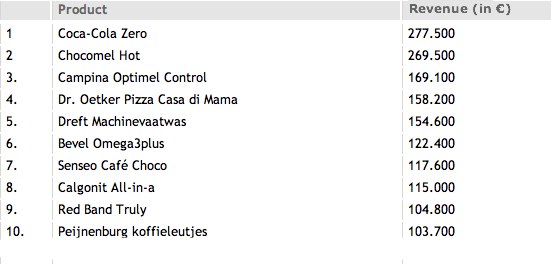

According to Distrifood.nl (Dutch) the " man's cola" showed a nice profit this last year, making it the top new introduction to a brand in 2007.

(Source picture: Elsevier.nl (Dutch))

I only point this out, since Coke Zero is one of the first food-related topics I wrote about on Tech IT Easy; a, fairly clear, signal that it was time to "spin-off" to this blog.

An interesting quote from the Economist this week. Particularly, because I personally suffer from it, and imagine a lot of other people & businesses do too.

An interesting quote from the Economist this week. Particularly, because I personally suffer from it, and imagine a lot of other people & businesses do too.

Mr. Fellows [CEO of Callaway golfing equipment] believes that the "fundamental principles of running a company don't change just because the product category is different." In his view, Callaway's problems stemmed from the fact that it saw itself as a golf business, not as a consumer-goods company. He resolved to focus on "what the consumer wants, not our own feelings about what the game of golf should be."It doesn't matter if you're the CEO of a company, an investor, a sales-person, a blogger, etc., I think everyone has an idea of what they want and what customers should want. But what it really comes down to is the latter.

Face Value, my favourite section in the Economist, every week.

The picture is courtesy of digitalfreak.net

Hey, a little busy at the moment, but here's some links, I've enjoyed recently.

Hey, a little busy at the moment, but here's some links, I've enjoyed recently.

- Jim Donald's, former Starbucks' CEO, month by Patricia Sellers (Fortune): After listening to an interview with Frank Addante on Venture Voice, where he said "Time is a finite asset!", I looked up "time-management CEO" on Google, and this is the first thing I found. Some good tips on meetings, getting up at 6, and generally managing your time.

- Monocle design-notes by Dan Hill: I printed this 32-page (!) document out this morning, and it will probably take me a few days to digest it, but I'm already enjoying the first few pages, where he writes about the vision behind Monocle as a mag. and as an internet-publication and how the multi-disciplinary team reflected this.

- 10 Ways to Improve Your Programming Productivity by Matt Moore: I love productivity-stuff, and think most of these tips apply to any activity really.

- The 7th Deadly Claim — “Best Value” by Jeff Sexton (Future Now): "The problem for most companies is that they don’t do BOTH well: Either they don’t do enough to persuade customers of the product’s value, or they price their high-quality item even higher than what they’ve been able to substantiate to the market."

- How Facebook Is Like Ikea by Tim Harford (Slate): Considering I wrote about something related a few months ago…

Normally, you would say that alcohol & money don't mix. But in the world of beer, at least in the Netherlands, there is tangled web that has been woven between financiers and the horeca-industry, which is difficult to unwind, and, some people argue, shouldn't be unwound.

Normally, you would say that alcohol & money don't mix. But in the world of beer, at least in the Netherlands, there is tangled web that has been woven between financiers and the horeca-industry, which is difficult to unwind, and, some people argue, shouldn't be unwound.

First of all, what is investing all about?

It's all about profit, obviously, but it's also about minimising the risk for investors. Two big risks facing investors are informational.

One the one hand, there's moral hazard—the risk that entrepreneurs take their new assets (money) and misuse it in some way; On the other hand, there's adverse selection—the risk that entrepreneurs are not as capable as they claim to be.

Either of these situations requires a different response and a different type of investor. For moral hazard, the typical response is for investors to mingle in the affairs of their investee's operations and strategy and take equity; the so-called active investor, which includes business angels and venture capitalists.

For adverse selection, the typical response is to restrict the entrepreneurs movement through collateral, restrictive, covenants, and and short maturities, to minimise risk-engaging behaviour. This is the realm of the passive investor, which includes banks.

Financial beer-tactics

When looking at these two investors, you see some differences; Active investors take equity—become part owner of the firm—and they do this because they can't do much else to influence the use of their money. Passive investors prefer to use measures like lend against collateral, e.g. real estate or other tangible assets, which they can claim if the investment were to go wrong.

In the case of horeca-owners, you typically do have some kind of physical asset. You occupy a venue, you have machinery, and inventory. This is much more the realm for passive investors, who can relatively safely lend some money against the existing collateral.

There is one complication, however; Horeca is typically known for high failure-rates. I'm not sure why this is so. I guess that the leisure industry is largely sensitive to seasonal differences and economic downturns. And perhaps, the barriers to entry are low; there could be a lot of low-skilled entrepreneurs out there, who are not as capable of running & growing a business as they think. And finally, growth in itself could be a problem, if the capital requirements are significant.

The way investors get around it in the Netherlands is actually not to invest. Instead, they leave it up to breweries, who, against a right of exclusivity, lend a certain sum to the business, or give it a discount, and provided it with the necessary materials, branded of course.

What's the problem?

From my angle, there isn't one really. If horeca is such a risky business, and other investors are unwilling to invest, then I don't think an entrepreneur should complain about a simple exclusivity-contract. And particularly so, because of three factors.

For one, exclusivity is only valid if the brewery has less than 30% market-share. In the case of someone like Heineken, who also owns a number of other beer-brands, and has more than 30% market-share, you can quit such a contract after two months. Then again, Heineken does its best to provide other value-added services to make sure that this doesn't happen.

And second, there's a lot of consolidation in the alcohol-business. And just because a company has a certain exclusivity, it may have such a large portfolio of brands that there isn't any shortage of choice for customers; neither do I think these exclusivity-contracts are 100% bullet-proof.

The third factor seems to be a problem. By not giving customers a choice, they have learned not to care about brand so much when they enter a pub. They just ask for a beer. So for them, unless they're a beer-fanatic, it doesn't matter much. For producers, on the other hand, their brand has become a commodity, at least where nightlife is concerned.

Who cares, right?

Heineken seems to care, and is all for the liberalisation of Dutch pubs. Ignoring that a. this would disrupt a pretty good funding situation for Dutch pubs, and b. that Heineken owns more than 30% of the beer-market, making their exclusivity-deals vulnerable anyway, I do kind of see their point.

By turning a brand into a commodity, you take away marketing-potential. If you can position your beer-brand above that of regular beer, then you can reap higher profits. That makes 100% sense to me, from the brewery's perspective.

And, from what I understand, British pubs don't actually have such exclusive deals with breweries. The question is then, how they get funded, or whether the failure rate is perhaps lower in the UK? That, for now, is a question unanswered to me, but I'll do my best to find out.

(You can always give it to me in the comments.)

Part of this topic was inspired by a good article (unfortunately not online) in Dutch Marketing Tribune, still my favourite Dutch mag.

When I started this blog, and my general thoughts about the area of food & retail, it was all about the people. A quality staff and happy customers, what more do you want? And I have to say, from past experiences, that I don't really like businesses that don't place people first.

When I started this blog, and my general thoughts about the area of food & retail, it was all about the people. A quality staff and happy customers, what more do you want? And I have to say, from past experiences, that I don't really like businesses that don't place people first.

For instance, one individual I worked with, suggested using handicapped people to put together a product manually. I instantly disliked him. Not that I don't want handicapped people to be productive, but it was the thought behind it; to find a "stupid" workforce, which you can save tons of money on. It was just distasteful.

Another company I worked for was very process-orientated.

There's nothing wrong with that of course, but it was a big company with a reputation for innovation and that is why I joined. And you expect such a company to at least push forward a solid project. Well, as it turned out, the organisation's core-strategy was to start a large number of risky projects and have them compete with each-other. Those that would fail would simply be abandoned, and their staff was expected to fall on their swords… metaphorically. The effect was an incredibly high turn-over of employees, all three projects I worked on no longer exist, and it deeply soured my feelings about this company.

Both these examples, to me, represent a lack of respect for the human element. I realise that business is a hard world, but if projects were designed to be solid in the first place, there would be less of a need for these kinds of practices. Just my 2 cents.

Part 2 - the challenges that people businesses face

HBR (Again! I'm sorry, but I read a lot of HBR-articles!) published an article about people businesses some time ago, which I enjoyed. Following are some notes + thoughts about it.

- People businesses are defined as: "operations which are characterised by 1. high overal employee costs, 2. a high ratio of employee costs to capital costs, and 3. limited spending on activities, such as R&D, aimed at generating future revenue."

- In a top-40 list of people-businesses, published in that same article, only a few qualify as food and/or retail related. These are the Hospital Corporation of America, Tenet Healthcare, Marriott hotels, and Accor hotels.

- For instance, a business like McDonalds does not classify as a people business; it has substantial assets in terms of brand & real-estate, and relatively low people-cost.

- People-businesses face a number of challenges, related to performance measurement, people-management, compensation, and business models.

- Measuring productivity is more important in these businesses, then other economic performance indicators, like return on assets or investment. The challenge is finding the right indicators (employee productivity & profitability), as well as benchmarking it against other companies (employee figures do not always need to be made public).

- To manage people, you need to align employees' interests with business objectives & execution. And you need to find ways to measure performance (see above) continuously and see where your weak spots are.

- Compensation is key, as productivity is very sensitive to it, and is a primary determinant of shareholder risks & returns. Other factors to consider are variability—productivity varies across the workforce and how do you get the most out of a diverse workforce—and reach—sometimes the lowest on the ladder are as, if not more important to a firm's performance, and how do you motivate these people to do their jobs as good as possible?

- There are a number of business models are used in these types of businesses: pricing per hour is a safe method, but does not account for extra performance; a fixed price per output allows companies to shave costs off the inputs and thus increase their profit-margins. It is very susceptible to a high-skilled workforce; a success-fee or commission offers the best returns, but also the greatest risks; some companies use a hybrid of these three.

- The strategic weakness with these types of businesses is that your assets are mobile and can walk out the door. By creating value above and beyond your employees, you can diversify some of that risk away. Of course, you could also try to keep your employees ;).

I guess it's up to individual businesses how they want to measure their firm's performance. The most straightforward is certainly return on assets or investment. But even that leads to some question-marks, particularly in today's highly software-based economy, where assets are no longer as necessary, or pricey, as they once were.

For my part, I still think that people are a key-asset to a business, and it's interesting to look at how exactly you motivate a workforce and get the most out of them, as well as how to overcome the challenges related to a people-based business.

Equally interesting is how to align the business-model to match the needs of your assets—the people. Since people are motivated by (financial & non-financial) compensation, do you keep the pay-rate aligned with time-spent; fixed; aligned with performance; or a hybrid of the three? I think the hybrid is always the best choice, but even then some combinations work better than others.

And retaining employees is also an interesting problem; though much less so in countries like France, where getting rid of them is a problem, and differently in places like Silicon Valley, where inter-firm mobility is a key-requirement for many employees. I think the solution is completely personal and cultural, and everybody's answer will be different on this.

The picture is courtesy of prairienet.org

I am not a born bootstrapper, let me make that clear from the start. I just like titles that include words starting with the same letter (is there a term for that?).

I am not a born bootstrapper, let me make that clear from the start. I just like titles that include words starting with the same letter (is there a term for that?).

Bootstrapping is, in my own definition, "the ability to generate growth on minimal financial resources." I was first going to call it "the ability to survive on minimal resources," however that would make most of the third world bootstrapping-geniuses.

No, it's when entrepreneurs have an idea that they want to grow into a commercial business, and since finding funding is difficult and less preferable for some, they do so with minimal financial means, perhaps while maintaining another source of income and by generating organic growth—revenues derived from within the company. In sociology, there is a concept called bricolage, which means more or less the same.

What makes a born bootstrapper, or rather a good one? I think it requires three qualities:

- The first is certainly the ability to live cheaply, and I'll refer you to one of Jeremy's post where he makes the point quite eloquently. The ability to live without luxury, eating at discounters, buying second-hand furniture (or dragging it off the street), living in cheaper areas, and, most importantly, to delay paying the bills, are certainly key-components here. As is, making resource-choices for your business. Easy to do when you work in software, less so in physical businesses, though inventory is fun to play around with.

- The second quality is time-management. You need to generate growth within your company and pay the rent, so you have to make choices. You have to find alternative revenue-streams, perhaps get another job, and work on your business during your free time. It requires you to set some clear priorities, skip the weekly cinema-visit or the time spent with your loved ones.

- The third and final quality, is to be goal-orientated. You could place that under time-management, perhaps, but where bootstrapping is most likely to fail is when motivation drops. You need to keep your eye on the ball at all times; the priority for a bootstrapper is to grow the business, not keep a stable job, and you need to see the light at the end of a tunnel and keep going until you reach it.

The picture is courtesy of rockies-ice.com

Read it on Tech IT Easy!

Read it on Tech IT Easy!

Ten tips, taken from an essay written by Masterson, entitled "The Winner's Rule", from the book "Just One Thing

Ten tips, taken from an essay written by Masterson, entitled "The Winner's Rule", from the book "Just One Thing

Advice is a funny thing. I don't think it's advice at all; rather it's a set of criteria or truths, and fairly shallow ones at that. They ignore the context a person, a reader, a student, a business goes through. And what if we all met these same criteria? Wouldn't the world be a much more boring place? As such, treat all "advice" with care.

I can classify Masterson's points into two categories: Business-related & person-related.

Business-related

1. It's not a business until you make the first sale.

2. The most effective way to enter a new market, is to offer a popular product at a drastically reduced price.

3. Sell, sell, sell: keep on increasing the perceived value, allowing you to ramp up the price, and increase profit margins.

All of these are sort of straight-forward, I think, though certain terms should be qualified. For instance, what does a 'sale' mean? It's easy to understand it within the context of a product going over the counter, but what about service-companies or the many web-businesses that fund themselves through advertising (if that)? I would nominate the first "rule" to be: It's not a business until you make money.

The second and third points, to me, seem like a typical VC-thing to say. Scale, scale, scale. Sell cheap and sell much. And worry about increasing the profit-margins later on. Again, it should be qualified, depending on the type of business. For instance, the internet is a market-place for countless cheap (or free) and mass-products; but as a result many products/services have become simple commodities, with no one willing to pay for them, and businesses having to look towards advertising as a funding-source (shudder).

Personality-related

4. When choosing a business, pick the one that can be grown without your personal involvement.

5. Before investing, know exactly how much you're willing to lose, and get out before you hit that point.

6. First, improve your strengths. Then, eliminate your weaknesses.

7. Focussing is more effective, than a diversified approach.

8. Let your winners run, and cut your losers off… quickly.

9. 80% of success comes from 20% of your resources.

10. Try to always focus on the good of the whole, vs. the good of the one (applies to any relationship).

Lot's more to say here.

Completely agreed with point four, as entrepreneurship should not be about enslaving yourself to another organisation, at least not for life. Many entrepreneurs seem to ignore that rule, however. Also, VCs often prefer to replace the founders with more qualified executives to "grow the pie."

Point five is spoken like an investor and is very much dependant on the perception of risk you have. Entrepreneurs are reputed to be risk-taking people, however the smart entrepreneur takes a calculated risk, and understanding how much you're willing to lose is part of that.

Point six and seven are a personal weakness of mine, I'm too damn curious for my own good sometimes, more interested in exploring areas (of myself or in life) that are unknown to me, rather than that which is known. That may change, but is certainly not a criteria that I personally meet. I wrote about focus before, btw. Differs from person to person.

Point eight comes with experience, I think. On the one hand, you need to have perseverance, even when things are hard or going badly, especially during the early stages of a start-up. On the other hand, a reality-check is price-less. I suggest bouncing your ideas off as many people as possible.

Point nine is true, nothing to add.

Point ten is about understanding the core-principles of business and, even as an employee, doing all you can to make that business (instead of yourself) profitable. Ram Charan is a good man to read on that.

Good essay, made me think about my place in the world.

Read more entrepreneurship articles here.

I just discovered a new podcast called "Big Ideas" (iTunes-link), a series of lectures on anything from the impact of urbanisation on musical tastes, to designing menus for restaurants. Oh, and it's Canadian. Not that that's bad, but some parts of the lecture covered local conditions.

John Schneeberger starts his lecture (dated March 1, 2008) off with the basics of menu-design, namely that they should reflect three things:

- What you stand for? Aka. what kind of food do you like to work with?

- What demographics are you targeting? Income, religious issues, etc.

- What are the current trends? And are they for real or just a fad?

- Customer-decisions are always a trade-off between price and quality

- Traditionally, dishes consist of three components: protein, starch, and vegetables.

- What we understand as taste, actually comes from three sources: fat, salt, and sugar.

Schneeberger discussed three booming trends, vegetarianism, organic food, and local produce, and mentioned a number of challenges related to these.

Vegetarian cooking

Vegetarian cookingThe thing to understand about this, is that it's generally cheaper. Schneeberger mentioned a 1:10 ratio when you compare the cost of producing vegetables to the cost of growing a cow. And while it's a booming trend, the industry, somewhat mis-guidedly, still often focusses on trying to replicate the taste of meat, which is impossible (think veggie-burgers, etc.).

Instead, they should be thinking about nutritional value— vegetarian food has been correlated with lower health-problems and is for that reason often recommended by doctors. The problem with these types of diets is of course that they are low in those qualities we would traditionally associate with taste: fat, salt, and sugar.

To create dishes that people actually enjoy, restaurants have to look globally, e.g. Asia, where more exotic vegetable components can bring some needed flavour to these dishes. I think he mentioned seaweed, but also stinky tofu (see pic), which is a type of fermented tofu and one of the few ways to naturally bring flavour to that type of protein.

The implication is that vegetarian food requires a significant amount of specialisation and is often hard to combine with meat-cooking.

Another complication arises from vegan (no dairy, honey, animal-derived products) versus lacto-ovo (incl. dairy, honey, animal-derived) cooking. The first makes it very hard to create a (traditionally) tasty dish. The second, lacto-ovo, allows for more flexibility, through the use of ingredients like eggs, which not only provide extra protein, but also bring a lot of flexibility to the kitchen. You can, for instance, make foam out if it, which would enable the creation of deserts & soups, etc.

Organic cooking

First of all (and I'm not sure if this is just restricted to Canada), an organic food label refers to the production method, not necessarily the quality and taste. Since organic food is more expensive, and taste is not guaranteed, you have to wonder if your clientele is willing to pay extra for that service (remember the trade-off between price & quality!).

The big selling-point here is the information about the product. People like to know how their food was produced; it has a certain value to know that there are no chemicals or genetically modified components in what you are eating. But again, that must be a value that is clearly advertised and which may not be important to every type of demographic.

Local produce

The advantage for the restaurant is that they can form better relationships with their suppliers, it's also cleaner in terms of carbon footprint (less transport), and it also has some marketing value to a certain demographic.

The disadvantage is that supply cannot be guaranteed during all seasons. Schneeberger mentioned something called a "100 mile diet" for instance, but restaurants catering to that need will probably have problems in the winter.

Thoughts

Overall, a pretty insightful lecture of the more exotic (and trendy) type of cooking and its trade-offs.

These types of specialisation are still pretty niche, require significant resources in terms of tools, know-how, and supplier-relations. But, if executed well, a niche can be extremely profitable.

I thought that it was interesting that all the traditional means of cooking, the ingredients and the taste-makers, were pretty incompatible with these newer trends. As such, you are essentially climbing up a hill, trying to educate the mass-market. At the same time, good execution, together with differentiation from the norm, seems like a formula for success.

This is as much a celebration of technologies like MixWit, which make publishing playlists (legally) possible, as it is a spotlight on one of my favourite musical discoveries last year.

Róisín (Pronounced "Roshiin") Murphy, former lead-singer in the British band Moloko, with a voice that reminds me a lot of Annie Lennox. I have to confess that, except for some remixes, I wasn't a big fan of either of these artists back in the day.

Still, Ms. Murphy is a breath of fresh air in what often seems like a stale and regurgitated pop-scene (I exaggerate). And… I simply can't get the first song on this playlist, "Dear Miami", out of my head!

Not for you, if you don't like electronica or pop.

Enjoy!

Just a short tweet.

Just a short tweet.

I'm currently reading a Dutch book on the 2003 crisis at Ahold, but which is actually a historical account of how the corporation came to be. A couple of things I found interesting:

- Ahold actually stands for AH (Albert Heijn) Holdings

- We all know that things are cyclical, but it was interesting to read how a recession and high oil prices were a challenge that Ahold had to face in the 60s-70s, and how they managed to survive.

- In order to inspire Dutch people to shop more, they introduced a financing scheme for fridges, which people couldn't afford at that time. General Motors did a similar thing to help people afford their cars; seems like an interesting way to "upgrade" an economy.

- The fear of a socialist government drove Albert Heijn to look outwards and form Ahold (similar to why IKEA decided to globalise also).

- One of the consequences of politics at that time was the board of directors, meant to provide impartial guidance and represent the workers.

- They made extensive use of consultancies (often McKinsey) whenever they decided on a strategic trajectory.

- One of the directors was a big fan of Harvard Business Review :)

- They use the US as a source of knowledge on how to design their supermarkets. Later on, moving to the US was also seen as a way to increase that learning, as well as a new revenue-source.

- When AH moved to the US, they also brought their own ideas, like, eh, advertising (a terrible, terrible idea).

I took this title from a report on the future of Dutch supermarkets (English pdf). It identifies a number challenges to come, one of which is "stomach share," which is apparently a big deal because of the following three factors:

- Population decline: which translates into less consumers buying food

- Increased longevity: and older people have a lower caloric intake

- Increased awareness of health-issues: which also translates to a lower caloric intake.

What the authors are seeing is that players from the bottom of the market (the discounters) are moving upwards, by broadening their assortment of goods, and players from the top of the market (luxury-stores) are moving downwards, by improving their prices. A number of underlying things are going on here: luxury-stores can become cheaper by improving the efficiency of their stores and sourcing cheaper brands. And discounters can increase their offering through their relationship with suppliers.

Following HBS-quote, from an article entitled "Finding success in the middle of the market", sheds some light how Tesco does it:

A company controls midfield by fielding a complete product line that includes backs and forwards. In its supermarkets, Tesco, the successful UK retailer, offers consumers three options—good, better and best—in most high turnover product categories. In addition, Tesco doesn't just sell groceries through one-size-fits-all supermarkets. Recognizing the need to shape as well as respond to an increasingly segmented market, Tesco reaches its consumers through at least seven different store formats, from convenient Tesco Express outlets at one end of the spectrum to full assortment hypermarkets at the other. But, within all its stores, Tesco implements the same merchandising principles: Better, Simpler, Cheaper.Can you guess who the loser is yet? Well, according to both the report and much data on the net, the losers are the new, innovative concepts, that may offer certain values to consumers on an ethical or health level, but are not able to reap the same advantages as more established players are.

That is also the answer why so many organic companies are being bought up by fmcg-companies. There's an interesting overview here; but if you want to follow one in real-time, check out this Inc. magazine blog run by Honest Tea, which has recently given away 40% of their company to Coca-Cola.

Of course that is only part of the answer. Consumers are not just focussed on price. And, while consumer-awareness of the global situation and their own health is clearly growing, that's not the whole answer either. People's lives are becoming ever more complex and convenience is a big selling point these days.

It's those companies that can combine a high level of consumer-responsiveness, together with assortment and price, that will capture the hearts of consumers. But I guess what is out, is the solo single-product-serving player in the market, purely focussed on softer advantages like "ethics," and forgetting that consumers still(!) have limited disposable income for their food-expenses, as well a limited time to engage in these activities.

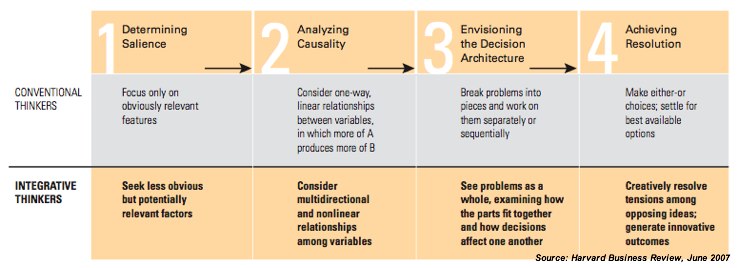

Entrepreneurial method: believe something is impossible? Enter 'double-think'

0 comments Posted by Unknown at 9:10 AMYesterday, I read an HBR-article by Roger Martin, on his book "The opposable mind", the ability for people to think contradicting thoughts and act on them at the same time (this may sound familiar, if you've ever read 1984).

My first instinct was to throw it out. I didn't like that he used the first few paragraphs to discredit other thinkers on leadership; and I didn't find his proposed method for coming up with a business-model particularly compatible with the general idea of "chaos" that he was proposing (more on that later). I even wrote an impassioned article about it, but waited a day before publishing it (no April fools from me this year). None of my criticism was directed at his core-concept, btw., I do believe in the ability to think contradicting thoughts, and act on them also.

After a night of sleep, I came to the conclusion that Martin's article was effective. Because it required me to think the article had faulty qualities, while the core-idea was right. And that was the very idea of 'double think'! Then I started thinking, what other areas could you apply this to? Pick one!

- My perception of the internet is that it's indiscriminately linear—we forget things the day after they are published. So how could you make it less linear?

- The perception of food is that it doesn't do well in e-commerce—they perish and people value touch. So how can you sell food via the internet?

- My perception of restaurants is that it requires a genius cook, who is both expensive and hard to handle. So how can you start a restaurant without such an individual, or better yet, how can you start a restaurant with one?

Martin's method for coming up a business-model looks like this:

In other words, you need to identify your core-customers, understand that their decision-process is not linear; understand the equally multi-dimensional architecture of your business, industry, and economy; and come out with a product/service that meets these opportunities.

Whether this is the best way to come up with an impossible idea, I'm not sure. But it seems like a logical thing to do after you come up with an idea and are looking to place it within a commercial context.

He uses one example throughout the article, that of Red Hat Linux, which, I completely agree, is one of the best examples to choose. It is free software, but it's a commercial success, which goes against conventional thinking, at least at that time. And instead of just acting as a commodity or becoming proprietary charge-ware, they decided to make a services-company out of it, and a market-leader at that. So how would you turn your open-source product into a commercial success? If that isn't 'double think', I don't know what is.

The

The