Essentially private labels, also sometimes called house brands, are products branded either with the name of the retailer, or, at times, sharing some kind of umbrella-name, decided by the distributor or otherwise. But what private labels really represent, to me, is the ultimate example of a power-struggle between a retailer and suppliers. Sometimes, but not always, it also means that some kind of vertical integration has been taking place between retailers and manufacturers, or, at the very least, packaging plants.

For now, I'll just be looking at some stats on private labels. At a later date, I'll take a look at more supplier-retailers dynamics, branding strategies, etc.

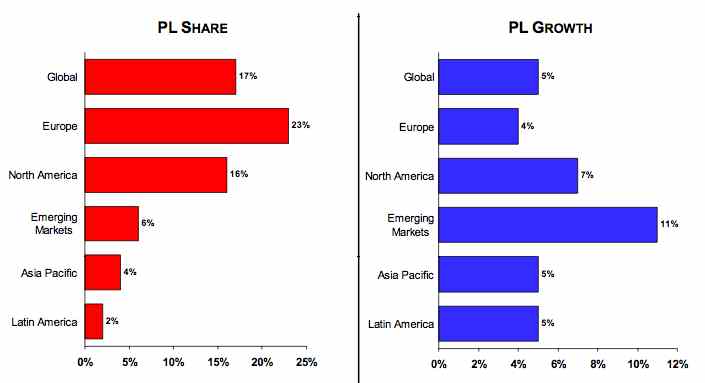

Geographic share

According to an ACNielsen report (pdf), the global* market-share for private brands was 17% in 2005 (* global meaning 38 countries and 80 categories), and had grown 6% that year.

Figure 1: Share & growth rates of private label by region (based on value sales) (source: ACNielsen, 2005)

Europe has the largest market-share with 23%, and Latin America the smallest, with 2%. Top countries included Switzerland, with 45%, Germany, with 30%, and the UK, with 28%. The largest Private Label growth happened, unsurprisingly, in emerging markets (11%) like Croatia (77%), Greece (24%), and Thailand (18%).

One big growth-contributor in Europe is the strong growth of hard discounters, such as Aldi or Lidl (both German chains), who are present in every European country and expanding rapidly. With Aldi, for instance, private labels make up 95% of sales.

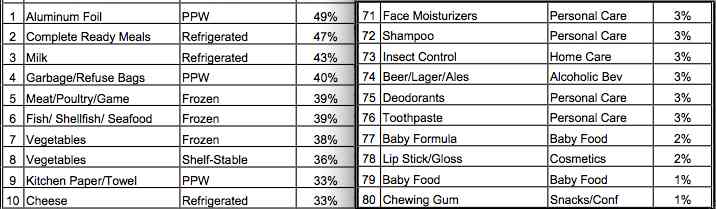

Private label foods

Category-wise, refrigerated foods have the largest overall share of private labels, namely 32%. Complete ready meals take the lead here, with an average of 47% private label-share. In the UK, 97% of ready-meal sales are in fact private label.

Another significant private label food, or rather drink, was milk, of which private labels make up 43% of sales.

Figure 2: Value shares of private label by category (source: ACNielsen, 2005)

Other high private label food-products include frozen meat (39%), fish (39%), and vegetables (38%), and 37% for shelved vegetables. Frozen pizza is at number 27, with 17%, tea and coffee at numbers 37 and 38, with 14% and 13% respectively. Wine is at number 44, with 12%. And Beer is all the way at the bottom, at number 74 with 3% !

Among the fastest growing foods are drinking yoghurt (28% growth), baby food (20%), chocolate (13%), and water (13%).

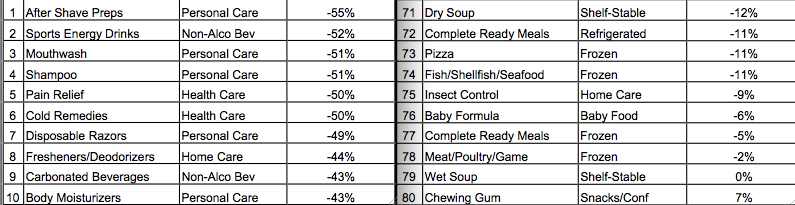

Pricing trends

One of the strengths of private labels is of course that they are cheaper, on average 31% less than manufacturer brands. Emerging markets showed the biggest discount, with PL-goods costing 41% less on average. Europe wasn't lagging in this respect either, with an average price difference of -37%. On a country level, Greece, Australia, and Germany were taking the lead with, respectively, -48%, -47%, and -46% discounts (compared to manufacturer brands).

Figure 3: Price differential of private label by category (source: ACNielsen, 2005)

Again, concentrating on food-categories, the products that received the biggest discounts were Sports Energy Drinks (-55%), carbonated beverages (-43%), cereals (-40%), wine (-38%), and tea (-37%). Food-categories taking the least in discounts, included chewing gum (+7%), wet soup (no difference), meat (-2%), and ready meals (-5% <- I guess that explains their high market-share).

Final thoughts

That market share is increasing more quickly in emerging countries is not surprising. Retailers there will likely not be mature and/or consolidated enough to focus on such a strategy, but this is clearly changing.

Germany's dominance is also interesting, as both Aldi and Lidl originate from there. One of my next posts will be on Ikea's European growth and Germany's also very strong there, which suggests a certain preference for low prices with German customers.

Switzerland is still somewhat of an enigma, but I'll try to find out more about it.

In terms of products, both the dominance of private labels amongst ready-made meals, and that their prices are quite similar to regular brands, is very interesting. It could suggest that customers either don't care much for quality and brand-differentiation in that sector, or that private label brands are actually quite good. The price-level would suggest the latter conclusion.

Generally speaking, refrigerated goods are different in the eyes of consumers, I think, less scrutinised perhaps, and worthy of more investigation. Milk is of course similar to water, and hence not really a product where brand makes a huge difference.

What else? Certain beverages, like coffee, wine, and beer are quite interesting, as their private label share is quite low. This would suggest a high brand-sensitivity in these sectors. The low percentage for beer (3%) is certainly striking.

More on private labels as I come to it.

Subscribe to:

Post Comments (Atom)

About this blog & the author

The S+FnR blog takes a look at the world of food-, retail-, and music-venues, and focusses on the following issues:

The S+FnR blog takes a look at the world of food-, retail-, and music-venues, and focusses on the following issues:

Setting up a business in this area * innovative practices and content * the marketing of ideas, values, products, services, locations, etc. * logistical considerations * mapping the value chain of the industry * sharing values through an organisation * attracting talent * motivating staff * integrating technology where possible * effective design * product and service choice * implementing social responsibility within and without the organisation * factors influencing location-choice * effective market-research * effective business planning * attracting finance at early and later stages * understanding taste * understanding experience * telling stories * more as this blog evolves.

Vincent van Wylick is the author of this weblog. You can find out more about him via his site, linkedin, his work on Tech IT Easy (a tech-blog), and his personal blog about philosophy, travels, and life-stuff.

For info or feedback, please send a mail to: foodandretailblog@gmail.com

Blog-Tools 4 U

Recent posts

-

▼

2007

(100)

-

▼

November

(25)

- Interlude: Sort of the way my thesis is going

- Interrupting my blogging-schedule for 12 days !!

- Starbucks' wholly-owned growth vs. Subway's franch...

- Private Labels II - thoughts about trends and patt...

- Random interlude - Imax, Guinness, pie

- The business of HoReCa - "Hotels, Restaurants, Cafes"

- Private Labels - a first look

- Interlude: Kill the Argument

- Media-interlude: food, sex, and… Axe !?

- Amazon's Jeff Bezos on strategy & innovation (not ...

- Meta-FNR II - meet Mr. Generalist

- Meta-FNR - Stuff I still need to do

- 5 Links: human sigma, link-baiting, neuroscience, ...

- Media-interlude: how to demolish a building Las Ve...

- Real Estate Strategy III - different types of costs

- Interlude: Malcolm Gladwell on people

- SEPA (Single Euro Payments Area) coming soon!

- IKEA's growth part I - the Scandinavian years

- 5 links to think - on Japan, designing experiences...

- Real Estate II - thinking about competition

- Interlude: The "10,000-hours-to-be-an-expert" rule

- Thinking about Real Estate - holistic approach & c...

- Bearish on the organic boom

- Media-interlude: digging Candy Dulfer's Sax

- Interlude: Technology-inspired Hiatus

-

▼

November

(25)

Latest Comments

Useful for you

Friends

- Cecil Dijoux on pop-culture

- DJ Utopianmind's (Nico) Goa-tunes

- Fidji Simo on tech, art, & biz

- Ivo Hop's free documentaries repository

- Jens Schriver's & Maximo Migliari's Cheathouse

- Jeremy Fain's & Friends' Tech IT Easy

- Leonard Sellem on web-media (FR/UK)

- Matthias Schwenk on Web 2.0 (DE)

- Stephanie Iguna's travelblog (FR)

- Vincent de la Mar on e-business 2.0

Labels

- About (23)

- Ahold (1)

- Amazon (5)

- Apple (4)

- Asia (6)

- beer (1)

- beverage (2)

- blogging (26)

- books (19)

- branding (47)

- business angels (2)

- business strategy (94)

- café (4)

- career (20)

- catering (25)

- Children (1)

- cinema (4)

- Coca-Cola (4)

- coffee (12)

- community (29)

- cooking (4)

- culture (63)

- customers (47)

- design (44)

- Disney (2)

- e-commerce (15)

- ebay (2)

- eco-trends (11)

- entertainment (28)

- entrepreneurship (78)

- ethics (24)

- Europe (26)

- farming (5)

- fashion (1)

- finance (23)

- fmcg (2)

- food (52)

- Franchising (11)

- geography (7)

- Globalisation (34)

- green (12)

- Health (9)

- Hennes and Mauritz (1)

- horeca (18)

- hotels (2)

- human resources (41)

- humour (19)

- Ikea (9)

- innovation (57)

- interlude (45)

- Jacques Brel (1)

- La Place (1)

- Legalese (2)

- Leonidas (2)

- Links (14)

- logistics (26)

- management (50)

- marketing (58)

- Marqt (1)

- mcdonalds (6)

- media (34)

- Milner (1)

- Monthly recap (5)

- music (18)

- Nestle (2)

- neuroscience (1)

- new business development (21)

- news (5)

- operation (13)

- operations (46)

- organic (5)

- Politics (8)

- private labels (3)

- real estate (14)

- Research (44)

- restaurants (26)

- retail (183)

- RFID (2)

- self-development (37)

- SEPA (1)

- snacks (1)

- starbucks (12)

- subsidies (4)

- Subway (2)

- supermarkets (14)

- suppliers (21)

- supply chain managment (24)

- Tchibo (1)

- technology (35)

- third place (2)

- tools (23)

- tourism (1)

- trends (52)

- Unilever (1)

- USA (21)

- venture capital (7)

- vision (46)

- Walmart (3)

- Wine (1)

- Zara (1)